KE

KE

NEWS

Insurance in Kenyan Schools: Uptake in Primary and Secondary Schools – 2025 Report Highlights

In recent years, Kenya has seen a rise in school-related disasters, especially fires. These events have caused property loss and damage to school buildings. They also show the need for insurance for these structures. Sadly, there have been injuries and even deaths. The country’s insurance industry has many affordable products for schools. However, most schools are still uninsured or underinsured. The 2025 report from the Association of Kenya Insurers (AKI) highlights this growing risk and urges quick reform.

In this article, we look at the main insights, statistics, challenges, and recommendations from the report. We explain why improving insurance coverage for schools is not just necessary, but urgent.

School Fires on the Rise: The Grim Reality

From January to September 2024, the Ministry of Education reported 107 school fire incidents. One tragic event was at Hillside Endarasha Academy, where 21 students lost their lives. In response, the government mandated a nationwide audit, leading to the closure of 348 boarding schools deemed unsafe.

On one single day in September 2024, 10 school fires were reported across the country. These incidents are a wake-up call: schools must prioritize risk mitigation—and insurance is a key part of that.

Insurance Uptake: A Disappointing 14.6%

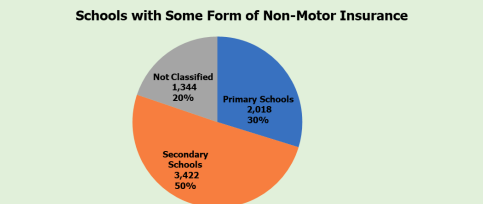

Kenya had 46,322 primary and secondary schools as of December 2023. However, only 6,784 insured schools—or 14.6%—had any form of non-motor insurance coverage in 2024.

Breakdown:

- 2,018 primary schools (30%)

- 3,422 secondary schools (50%)

- 1,344 schools had incomplete data(20%)

This leaves over 85% of schools exposed to risks that could otherwise be mitigated through affordable insurance policies.

Insurance Products Offered to Schools

Of the 34 insurers surveyed by AKI:

- 32 companies provide insurance products for schools.

- Most common products include:

- Fire & Special Perils – 32 insurers

- Group/Student Personal Accident (GPA) – 29 insurers

- WIBA (Work Injury Benefits Act) – 27 insurers

- Burglary/Theft – 27 insurers

- All Risks – 20 insurers

- Public Liability – 18 insurers

Some insurers offer medical insurance for schools. This can cover medical visits and costs after serious illnesses like cancer are diagnosed.

Specialized covers like Fidelity Guarantee and Political Violence exist but are less frequently offered.

Employer Liability and Compliance

Employer liability is a cornerstone of responsible school management in Kenya. Under the Work Injury Benefits Act (WIBA), schools must provide insurance for their employees. This covers work-related injuries, disabilities, or deaths. Every school must have the right insurance products. This includes a Group Personal Accident policy. This policy protects teachers and staff from unexpected accidents and permanent total disability.

Following the rules of the Insurance Regulatory Authority (IRA) of Kenya is not just a legal step. It is important for protecting the school’s money and reputation. By following IRA guidelines and keeping insurance coverage current, schools can avoid expensive liability claims. This helps ensure that any incidents are handled efficiently. In an accident, having the right policy helps claims get processed quickly. This provides support to affected staff and their families.

School Transportation and Insurance

Safe and reliable school transportation is essential for students’ well-being. Schools can get full insurance coverage for their buses and vehicles. This protects them from risks like accidents, fire, and theft. A good insurance policy covers repair or replacement costs. It also offers third-party liability coverage for injuries or deaths from transportation accidents.

To make their transportation services safer, schools can add more safety measures. They can use CCTV cameras and GPS tracking systems. This will lower risks and improve the overall safety of students. Schools can focus on insurance for transportation. This helps them reduce claims. It also protects their assets. Most importantly, it keeps students safe every day.

Directors and Officers Liability

Directors and Officers (D&O) liability insurance is a critical safeguard for school leadership. This policy protects directors, officers, and board members from personal claims. These claims may come from decisions made during their official duties. D&O insurance protects school leaders from personal liability. This applies to claims about employment practices, student safety, or financial management. It ensures they are safe when acting in good faith.

A public liability policy can protect schools from claims about injuries or deaths due to negligence. It offers broad coverage for many possible incidents. By getting D&O and public liability insurance, schools can protect their leaders. This helps them keep good governance. They can focus on providing quality education without worrying about personal financial risks.

Barriers to Insurance Adoption in Schools

1. Low Awareness

Many school heads and boards lack a basic understanding of insurance or its benefits. Insurance is wrongly viewed as optional, with a false reliance on government or community bailouts during disasters. Schools and insurers must find effective ways to communicate the benefits and processes of insurance to all stakeholders.

2. Budget Constraints

Most schools—especially public ones—operate on minimal budgets. Without a formal budget for insurance, schools often ignore it. They focus on daily needs instead. This makes it hard for them to pay insurance premiums. It is especially tough when they must pay in cash and have few other payment options.

3. Weak Risk Management

Not having fire extinguishers, emergency exits, or updated asset lists is a problem. It makes it difficult to get the right insurance policies. It also makes it hard to make successful claims.

4. Distrust and Poor Perceptions

Past negative experiences, such as delayed claim payments or unclear processes, have led to mistrust among administrators. Having dedicated personnel to assist schools with claims and insurance processes could help address these negative perceptions.

5. Market Conduct and Accessibility

Problems like undercutting, unregulated incentives, and complicated procurement make insurance hard to get. This is especially true in marginalized areas. These issues create extra challenges for insurance intermediaries who help schools find the right coverage.

6. Lack of Regulatory Mandates

Currently, no law requires schools to have non-motor insurance. The Ministry of Education’s Safety Manual gives general safety guidelines. However, there is no enforcement or funding for insurance. However, some associations have been formed to advocate for stronger insurance mandates in schools.

Key Recommendations from the AKI Report

1. Increase Awareness and Capacity Building

- Roll out regional sensitization forums, workshops, and school visits.

- Use simplified brochures and proposal forms.

- Partner with the Ministry of Education for national coordination.

2. Integrate Insurance in Policy and Regulation

- Introduce minimum mandatory covers such as Fire, WIBA, and Student Accident Insurance.

- Include insurance allocations in both public and private school budgeting guidelines.

3. Develop Tailored, Affordable Products

- Bundle critical covers into one simplified policy.

- Introduce term-based or installment payment models.

- Standardize affordable rates—especially for fire insurance—to improve access.

4. Strengthen Risk Management Support

- Conduct safety audits and help schools meet minimum risk standards.

- Provide first aid and safety training for staff.

- Incentivize schools with good safety records.

5. Leverage Technology and Digital Access

- Promote mobile insurance and digital policy onboarding.

- Simplify renewals and communication through mobile-friendly platforms.

- Improve oversight of agents and brokers to eliminate unethical practices.

6. Foster Partnerships and Collaboration

- Encourage collaboration between AKI, MoE, county governments, and education associations.

- Align insurance planning with the school calendar and national education budgets.

- Support schools in explicitly budgeting for insurance in their annual planning.

- Foster partnerships with financial institutions, including those that have a wholly owned subsidiary dedicated to providing insurance services.

Future Outlook and Trends

The future of insurance in Kenya’s education sector is marked by innovation and growth. As digital transformation is changing the industry. Online platforms help schools get coverage, manage policies, and file claims more easily. This increased accessibility helps schools get their funds, protect their assets, and keep things running during unexpected events.

In the future, partnerships between schools, insurers, and government agencies will be important. They will help achieve complete risk protection for all schools in Kenya. Schools can stay updated on market trends. They should work with reliable insurance providers. This helps protect their students, staff, and resources, creating a safe and successful learning environment for future generations.

Why Schools Must Act Now

The spate of school fires and the growing scale of uninsured risk cannot be ignored. Insurance provides an important safety net. It helps keep education going, protects school buildings, and offers compensation after accidents or disasters.

Without insurance:

- Parents bear the rebuilding costs, including the loss of money due to theft or damage not covered by insurance

- Learning is disrupted for months

- Injured students and teachers lack adequate support

- Schools face reputational damage and legal liability

Conclusion: Safeguarding Education with Smart Risk Protection

The 2025 AKI report provides clear evidence that Kenyan schools remain dangerously underinsured, despite the growing risks they face. A multi-stakeholder approach is important. It includes the insurance sector, government, and school management. This approach helps improve awareness, trust, access, and policy uptake. Investing in school insurance is not just smart; it is essential. It helps protect students, staff, and Kenya’s education system.