KE

KE

NEWS

Motor Trade Insurance Kenya: Protect Your Auto Business

Operating a vehicle dealership, import clearing service, or mechanical workshop in Kenya is a high-exposure venture. Unlike businesses that deal with static inventory, an automotive business handles mobile, high-value assets belonging to both the company and its clients.

When a vehicle enters your business ecosystem, it moves through different legal and physical states. A standard private or commercial motor vehicle policy fails in this environment because it links coverage to a single registered vehicle and specified drivers.

To protect your business from catastrophic cash-flow shocks, you must understand Motor Trade Liability—the specialized legal and insurance framework that governs businesses handling vehicles they do not personally own.

1. The Legal Framework: “Care, Custody, and Control” (Bailee Liability)

When a customer leaves their car at your garage or yard for repairs, servicing, or detailing, you create a legal relationship called bailment. Your business becomes the Bailee, and the customer is the Bailor.

Under Kenyan common law, a bailee owes a strict duty of care to safeguard the property in their possession.

The Legal Blind Spot: Many business owners assume that a standard Public Liability policy covers accidents on their premises. However, underwriters write a strict Care, Custody, and Control (CCC) exclusion clause into virtually all standard public liability policies. This means that if your team damages a customer’s car during a repair, standard liability insurance will refuse the claim because you held direct control over the property.

To bridge this gap, you require a specialized Motor Trade (Garage/Internal Risks) Policy. It specifically nullifies the CCC exclusion, ensuring that the policy covers internal operational hazards impacting customer vehicles.

2. Technical Breakdown: Road Risks vs. Internal (Garage) Risks

A comprehensive Motor Trade framework is split into two distinct operational covers. Understanding how these two policies interact prevents costly coverage gaps.

A. Road Risks Cover (Vehicles in Motion)

This cover allows your business to operate vehicles on public roads for business purposes without registering each vehicle individually on the policy.

The Regulatory Reality: KG vs. KD Plates

In Kenya, the National Transport and Safety Authority (NTSA) issues specialized, green-background number plates for the motor trade. However, the law distinguishes sharply between who can use them, and underwriters look closely at these designations during a claim:

-

KG Plates (Kenya Garage): NTSA issues these strictly to licensed garages, motor underwriters, vehicle assemblers, and body fabricators. You use a KG plate specifically to road-test a vehicle under repair, or to move a vehicle from one workshop bay to an external specialist (like an upholstery shop or alignment center).

-

KD Plates (Kenya Dealer): NTSA issues these strictly to licensed motor vehicle dealers and importers. You use a KD plate as a logistical tool to move unregistered import units from Container Freight Stations (CFS) or the Port of Mombasa to upcountry showrooms and yards, or to facilitate client test drives.

The Compliance Trap: NTSA regulations strictly prohibit using a KD or KG plate to carry passengers or goods for commercial profit. Furthermore, following system updates, NTSA requires dealers to log customs import entry details before generating a driver’s movement registry for a KD plate. If traffic police intercept a vehicle using a KD plate without matching portal documentation, or if a garage uses a KG plate for a simple dealership transit role, the authority can impound the vehicle, and your insurer will likely void any accident claim due to illegal vehicle usage.

B. Internal Risks / Garage Cover (Vehicles at Rest)

This functions as a specialized property and liability shield for your fixed physical location (the workshop, yard, or showroom). It covers:

-

Premises Liability: It handles compensation claims if third parties sustain injuries on your site (e.g., a customer slipping on a grease patch in a repair bay).

-

Material Damage: It reimburses you for damage to your physical infrastructure, computerized diagnostic equipment, hydraulic lifts, and hand tools caused by fire, flooding, or electrical surges.

-

Open-Yard Perils: It provides specialized protection against theft, vandalism, or fire for vehicle stock that you store out in the open (crucial for car yards along major thoroughfares like Ngong Road or Mombasa Road).

3. The 4 Most Critical Extensions Auto Businesses Miss

Standard off-the-shelf insurance policies often leave out specialized clauses that are vital for automotive operations. When structuring or auditing your business cover, ensure you explicitly include these four technical extensions:

1. Defective Workmanship (Consequential Damage)

If a mechanic improperly tightens a wheel hub assembly during a routine service, and that wheel comes off three days later while the client is driving on a highway, your business faces massive legal liability.

-

The Nuance: Insurance will never pay to fix the bad mechanical work itself (the poorly tightened bolt). However, a Defective Workmanship Extension will cover the resulting third-party bodily injuries, property damage, and vehicle destruction that the mechanical failure caused.

2. Loss of Use / Loss of Profits

If a fire inside your workshop severely damages a customer’s commercial delivery van, you owe compensation not just for the physical repairs, but potentially for the income that the business loses while you ground their vehicle. A loss of use extension shields you from these compounding financial claims.

3. Transit Risk (Port to Showroom)

For vehicle importers, the journey from the Port of Mombasa to upcountry showrooms involves high risk (hijackings, carrier rollovers, or stone-throwing damage). Standard road risks may only cover localized driving. Ensure your policy explicitly covers long-distance transit or pair it with a Marine/Inland Transit policy.

4. Work Injury Benefits Act (WIBA) Alignment

Garages and assembly workshops are high-hazard environments involving welding, heavy machinery, and volatile fluids. In Kenya, the law mandates that you cover your employees under the Work Injury Benefits Act (WIBA). Integrating WIBA with your overall garage policy ensures you cover your technicians for occupational injuries without duplicating your premium costs.

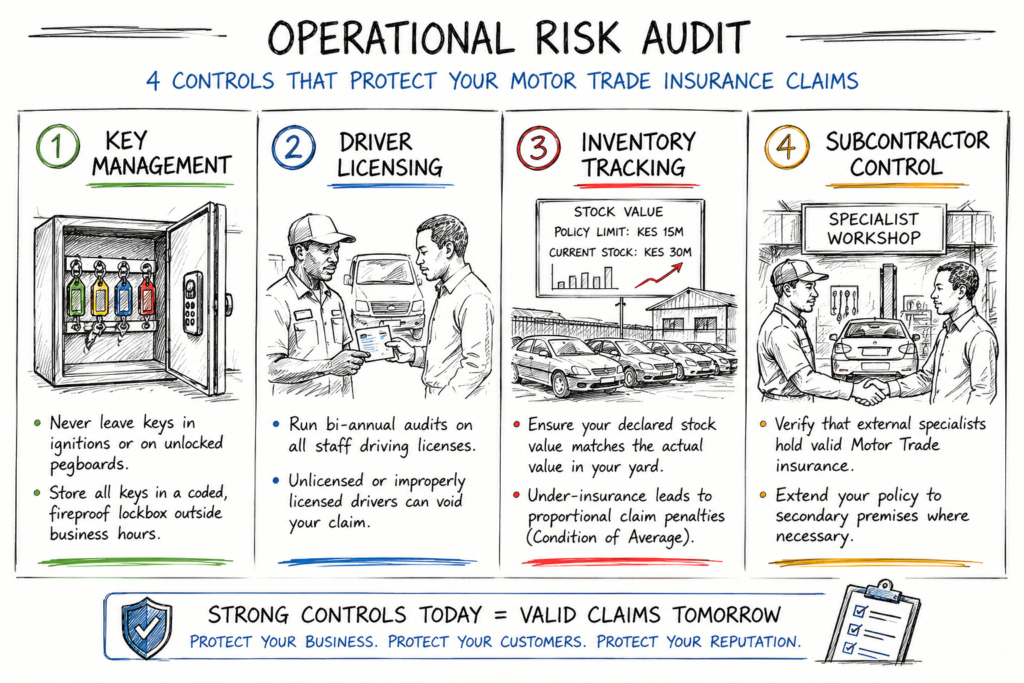

4. Operational Risk Audit: Protecting Your Claims Validity

Holding a policy document does not guarantee a payout. Insurance contracts rely on the principle of utmost good faith and require the business owner to take reasonable steps to mitigate risk.

Use this checklist to ensure your daily operations do not accidentally void your coverage:

Conclusion: Engineering Business Resilience

Smart business owners do not view Motor Trade Insurance as a bureaucratic box to tick or a marketing expense. It serves as a vital piece of financial engineering that prevents operational accidents from becoming business-ending liabilities.

By understanding the distinction between road and internal risks, eliminating the care, custody, and control blind spot, and maintaining strict on-site risk protocols, automotive business owners can ensure their operations remain resilient, compliant, and structurally secure against the unexpected.